The Rising Student Debt Crisis Hits Young Earners Hard

Rachel Reeves’ recent budget changes to the student loan system have ignited fierce criticism across Westminster and beyond. For millions who earned degrees in the 2010s—and their families—these reforms confirm what many have long feared: the student debt burden is escalating, squeezing young workers just as they enter their peak earning years.

With approximately five million borrowers impacted, the backlash is expected to intensify next month. That’s when the final round of inflation-linked repayment relief ends, and a three-year freeze on the earnings threshold kicks in, following Reeves’ announcement last November.

Understanding the Roots of the Student Loan Problem

At the core of this controversy lie the Plan 2 student loans, introduced in 2012 alongside a sharp tuition fee hike to £9,000 per year. These loans, offered until 2023, now account for 80% of England’s colossal £240 billion student loan debt.

Plan 2 repayments function like a tax: borrowers pay 9% of their income over a threshold—set just above £29,000 since April. However, unlike traditional loans, interest accumulates at the Retail Price Index (RPI) inflation rate, currently 3.2%, plus an additional up to 3%, depending on income. This makes Plan 2 loans significantly more expensive than the earlier Plan 1 loans.

The debt balance is wiped clean only after 30 years if it remains unpaid.

Policy Shifts That Have Worsened the Debt

Plan 2 terms have undergone frequent and costly changes. In 2022, Boris Johnson’s government added the extra 3% interest to the RPI rate and froze the earnings threshold. After a brief reprieve, Reeves reinstated the freeze, pushing repayments higher.

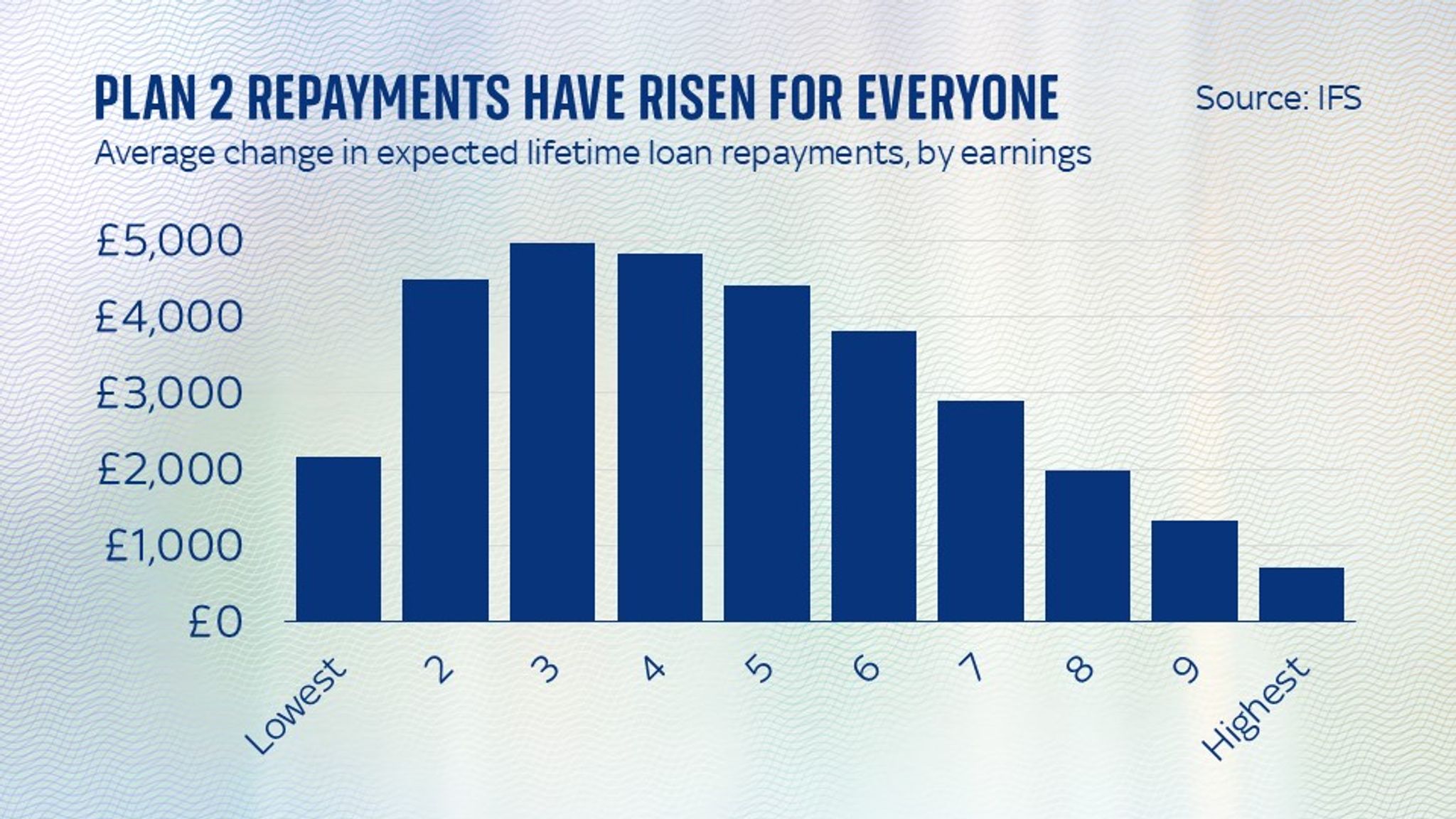

Why the Earnings Threshold Freeze Amplifies Repayments

The earnings threshold exists to shield lower earners from premature repayments, differentiating student loans from standard debt. By freezing this threshold, the government forces all borrowers to pay back more. The Institute for Fiscal Studies (IFS) estimates that average lifetime repayments will increase by £3,000, with low earners facing hikes as steep as £5,000, while the wealthiest see a rise of only £700.

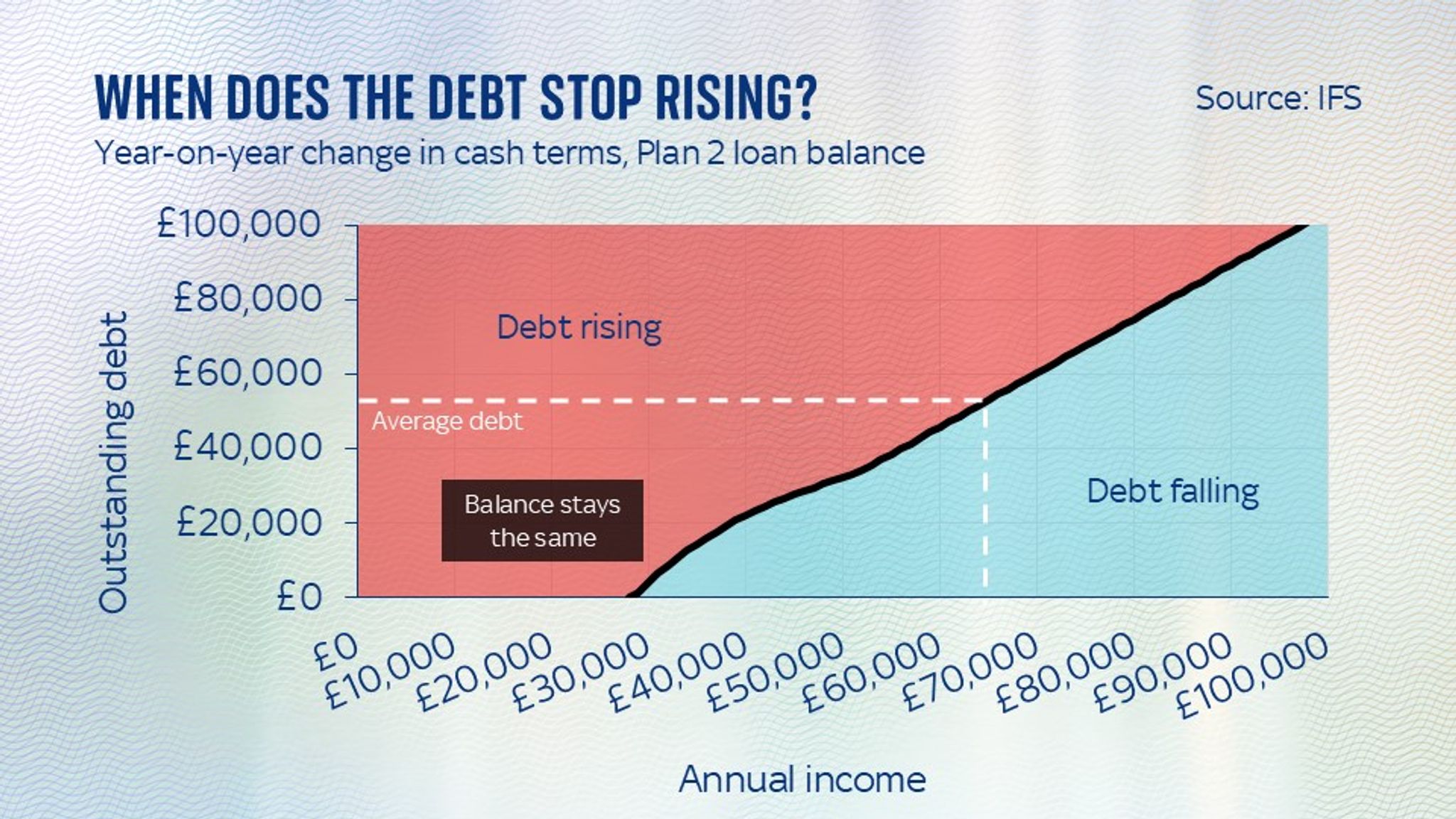

The Core Challenge: Debt Grows Faster Than Repayments

Most borrowers struggle to reduce their debt because the interest accumulates faster than repayments. Last year alone, £15 billion in interest was added to the student loan book, while only £5 billion was repaid.

Unlike fixed-term bank loans, student loan repayments fluctuate based on individual earnings. Two graduates with identical debt can end up repaying vastly different sums over their careers.

How Student Loans Fail Borrowers Across Income Levels

Rethink Repayments, a campaign group advocating for reform, has modeled repayment scenarios illustrating stark disparities:

- A low-earner starting with a £43,000 loan and a £15,000 salary rising to £85,000 will repay just £36,000, but their debt will balloon above £100,000 before being written off.

- A medium-earner with the same initial debt, earning from £21,000 to £110,000, will repay over £70,000 but only begins to reduce the principal after 25 years, with £90,000 eventually forgiven.

- A high-earner moving from £27,000 to £142,000 will pay more than £120,000—nearly four times the low-earner’s repayment—yet still won’t clear the debt completely.

The average graduate carrying £53,000 in debt must earn £66,000 annually before their repayments outpace the interest charged.

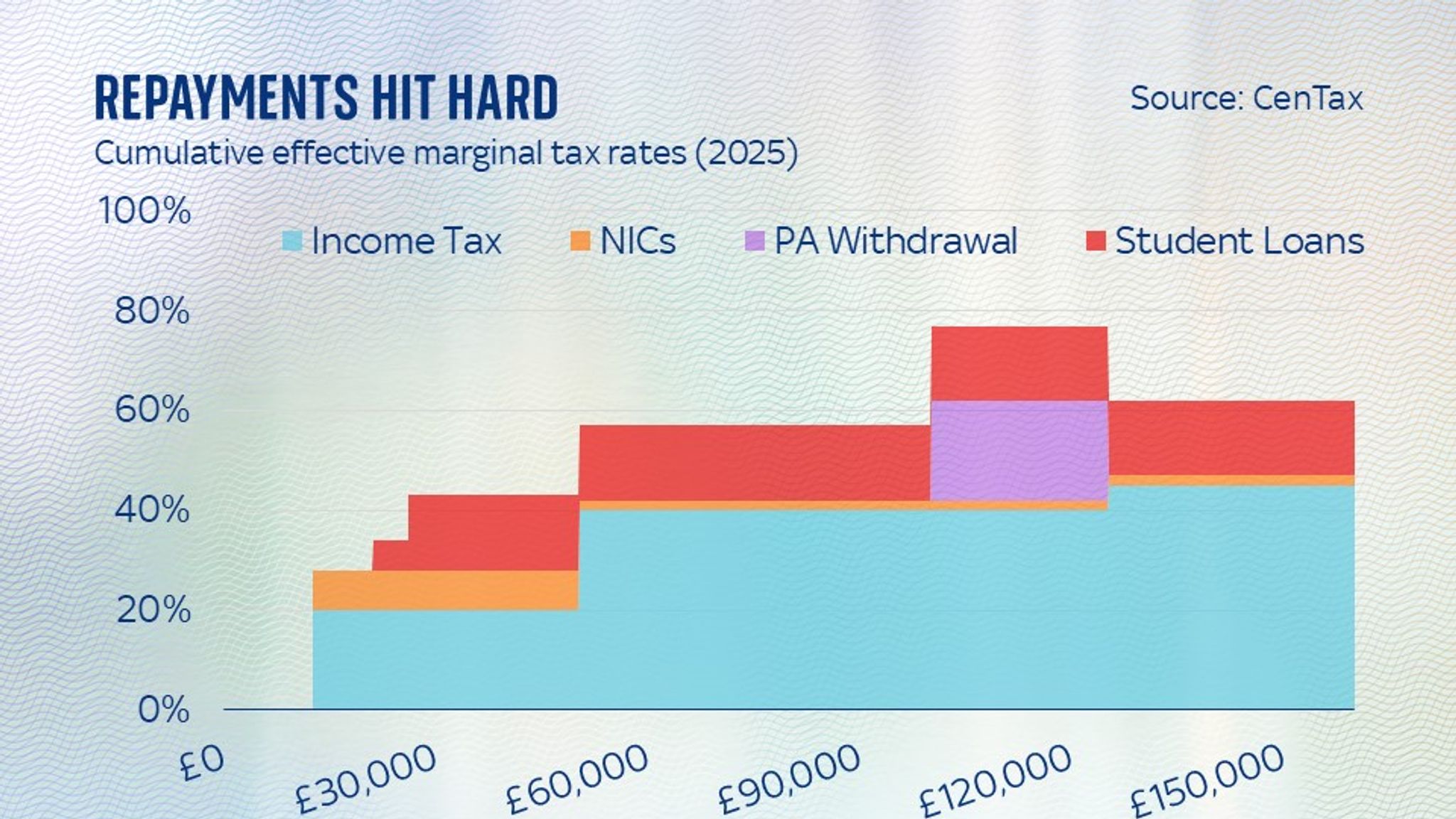

The Punishing Tax-Like Repayment Structure

Plan 2 loans act like a “graduate tax,” imposing harsh marginal tax rates. Once borrowers surpass the earnings threshold, they face a marginal rate of 38%, as the 9% loan repayment stacks on top of income tax and National Insurance. Crossing the £50,000 income mark triggers the higher tax rate, pushing their marginal rate to 51%, leaving graduates with less than half of every extra pound earned.

Combined with soaring housing and childcare costs, this financial squeeze leaves many graduates feeling trapped, despite having invested in a degree they hoped would secure a prosperous future.

Government Response and Political Stalemate

Despite the uproar, the government stands firm. Chancellor Rachel Reeves defends the changes as “fair,” while Prime Minister Rishi Sunak has promised to explore options for a “fairer” loan system. However, no official review updates have emerged, and the issue’s political priority remains uncertain.

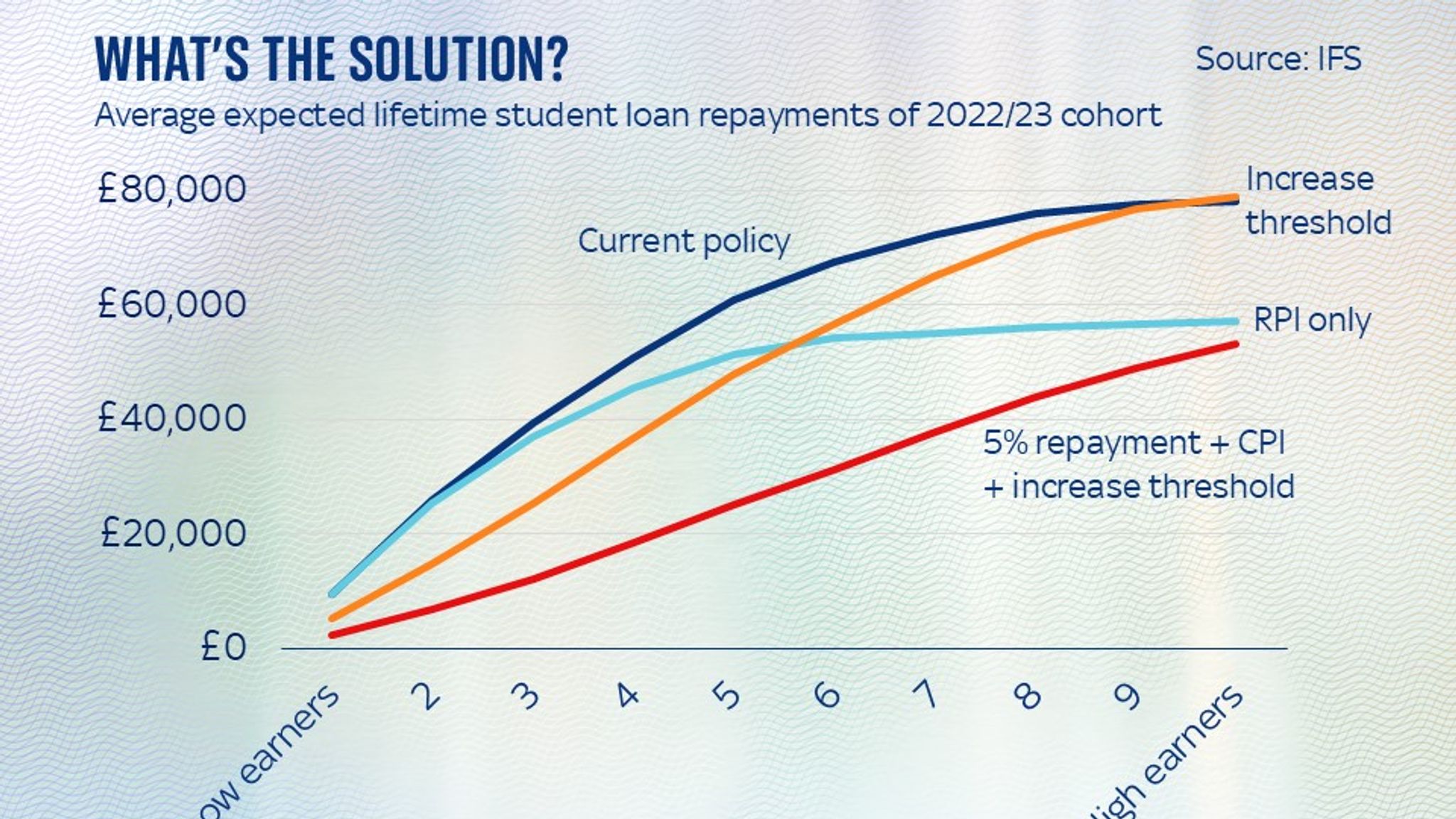

Potential Reforms on the Table

Opposition parties propose varying solutions:

- Conservatives seek to remove the extra 3% interest, reverting solely to RPI. This wouldn’t reduce immediate repayments but would cut lifetime costs by an estimated £3 billion.

- Liberal Democrats advocate raising the repayment threshold in line with average earnings, lowering payments now and long term, costing about £4 billion.

- Rethink Repayments recommends restoring the threshold, switching interest calculations from RPI to CPI, and halving the repayment rate to 5%. This would dramatically reduce borrower costs and require an estimated £11 billion in public funding.

While these proposals could ease borrower pressure and represent policy U-turns, none address the deeper challenge of funding higher education sustainably.

The Fundamental Dilemma: Who Should Pay for Higher Education?

Plan 2 loans were designed to place repayment responsibility on graduates rather than taxpayers without degrees, linking repayments directly to earnings. Yet, with many universities running financial deficits and relying heavily on overseas students to subsidize domestic tuition—which remains too low to cover teaching costs—the sector faces a funding crunch.

Without significant changes to how higher education is financed, the student debt crisis will persist, continuing to weigh heavily on the shoulders of graduates and the economy alike.